10 things you need to know about carrier billing

by Sukey Miller

![]() Identified as one MEF’s “10 Key Mobile Trends for 2015”, carrier billing is a major driver behind the global growth in digital content sales. Carrier billing enables consumers to buy apps, games, music and other content by charging the cost to their mobile bill, in one or more taps. Here, Richard Leyland, VP Marketing with Bango, the global leader in carrier billing, shares the 10 things you need to know:

Identified as one MEF’s “10 Key Mobile Trends for 2015”, carrier billing is a major driver behind the global growth in digital content sales. Carrier billing enables consumers to buy apps, games, music and other content by charging the cost to their mobile bill, in one or more taps. Here, Richard Leyland, VP Marketing with Bango, the global leader in carrier billing, shares the 10 things you need to know:

1. It’s happening now

Where many mobile payment technologies are known for expectation and hype, but disappointing revenues, carrier billing is a notable exception. It’s happening now, on a massive scale. As app stores have driven the digital content market forward, so carrier billing has grown and increased its share of the overall market. The global carrier billing market was worth around $4 billion in 2014 and is predicted to rise to around $13 billion by the end of 2017 (Juniper Research).

2. Mobile operators are using carrier billing to fight back

Revenues from voice and messaging are in decline for most mobile operators. Over The Top services (think Skype, WhatsApp, Instagram and Snapchat) are increasing data usage for the mobile operators, but those same services are destroying voice and messaging revenues. Carrier billing allows the mobile operators to fight back, and to gain a slice of the revenue that’s flowing over their networks anyway.

3. The giants of mobile are on board

The last two years have seen unprecedented momentum in the carrier billing market, as the leaders in digital content sales – the app stores – have embraced the technology. As Business Insider has pointed out, “Google has been cutting deals with wireless carriers everywhere”, while Microsoft’s Windows Phone Store has more than 80 live markets. The final months of 2014 saw Bango announce the introduction of carrier billing to Amazon Appstore and a global partnership with Samsung, to roll out carrier billing for users of Samsung GALAXY Apps.

4. Where is Apple in all of this?

Apple’s App Store is the only leading app store yet to embrace carrier billing. Apple stands alone in having built a huge mobile content ecosystem – valued in the tens of billions – based on credit/debit card sales. The thought remains though that if Apple seeks to build substantial digital content revenues in fast-growing, developing world markets, they may choose to support the universal payment mechanism of the phone and phone bill. Until that day…

5. Carrier billing sells more stuff

It’s all about the conversion rate. Offering a frictionless, one-click payment experience is proven to maximize sales, even in markets with high credit-card ownership. Analysis of Bango’s own payment data shows this effect. Where consumers are only presented with a credit/debit card only payment option, conversion rates can be as low as 0.5% in developing markets, and rarely exceed 40% even in developed markets where card penetration is high. The average conversion rate for carrier billing in app stores using the Bango Payment Platform during 2014 was 82.4% .

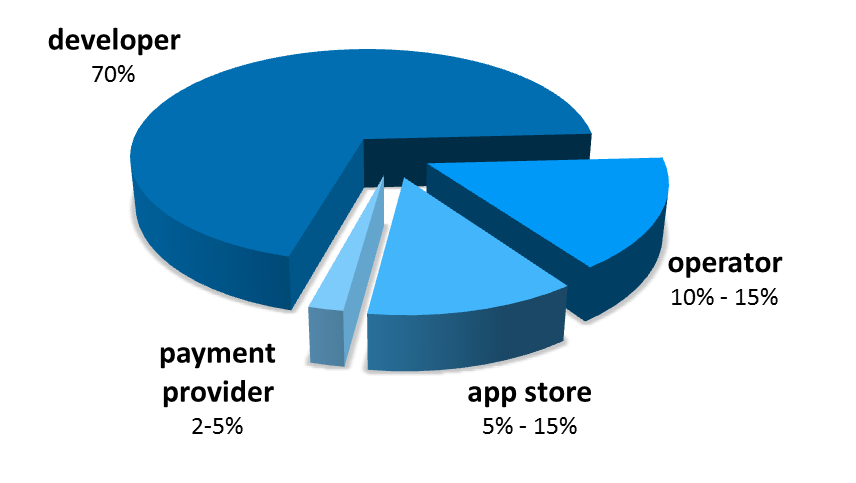

6. Where does the money go?

The 70% payout to mobile content developers is one of the few unchanging facts of the app economy. The remaining 30% is the subject of commercial negotiation, and tends to look something like this:

7. A word on margins

The operator’s glory days of mobile wallpaper, ringtones and huge margins are long gone. This is undeniably low margin business for mobile operators accustomed to taking the largest slice of the pie. Against that background, mobile operators are tending to outsource to specialist payment platforms that work at scale, handle complexity, capex, R&D and so on.

8. Not so “micro” payments

Average purchase values with carrier billing are probably higher than you think. In January 2015 the world’s highest grossing app in Google Play was the freemium game ‘Clash of Clans’, by Supercell. Players make in-app purchases for “Gems”, the in-app currency, in one of five different volumes:

“Pile of Gems” at $4.99 for 500 Gems

“Bag of Gems” is $9.99 for 1,200 Gems

“Sack of Gems” is $19.99 for 2,500 Gems

“Box of Gems” is $49.99 for 6,500 Gems

“Chest of Gems” is $99.99 for 14,000 Gems

And which is the most popular purchase? Not the cheapest $4.99 option. In fact the highest selling option is the $9.99 Bag of Gems. Bango sees twice as many Bag of Gems sold per day as Pile of Gems, earning the developer four times the revenue. Even in developing world markets, the highest grossing price points across the range of content (not just in Clash of Clans) are $4.99, followed closely by $9.99.

So forget 99 cents. These price points, rarely falling below $4.99, are the norm for carrier billing purchases.

9. Buyer beware : All carrier billing is not the same

‘Real’ carrier billing is achieved through a direct integration into the billing system of a mobile operator, allowing a charge to be placed on a phone bill. Some mobile payment providers boast hundreds of what they call “direct billing connections,” but in reality they are dependent on an inferior approach – Premium SMS – a fiddly, indirect and error-prone technology associated with payment error and scams. This “direct” billing is often a proxy through additional third parties, unknown to the merchant, to achieve high aggregate coverage. Premium SMS is all but banned in the USA and is being regulated out of existence elsewhere, but until its completely gone, caveat emptor – let the buyer beware.

For more information download Bango’s white paper “Beware of BOB”.

10. Carrier billing for physical goods

Various companies are exploring the potential of carrier billing for the sale of physical goods. Applications include using carrier billing for magazine sales, IT consumables, train tickets and more.

However these innovative applications for carrier billing remain at the margins. There are considerable complexities involved here, including the requirement for an e-money license. The regulatory environment for the purchase of physical goods is probably better matched to credit card, cash and banking service providers. In addition, mobile operators are acutely aware of “bill shock”, and may prefer that consumers push the upper limit of their bill with high margin messaging, data and calls, rather than lower margin physical goods. In short, it may be some while before we’re purchasing TVs and refrigerators on our phone bill…

![]()

Subscribe to our newsletter

Get the latest subscription bundling news and insights delivered straight to your inbox.