The subscription economy is reorganizing around the consumer

by Marta Trias Gray | 11 May 2026

There is a familiar moment, where you open your TV, move between a few apps, scroll through different services and still don’t settle on anything. According to data from Bango Subscription signals 2026, 29% of consumers spend more than 30 minutes browsing streaming services to decide what to watch, rising to 48% among Gen Z, yet after all that searching, many still don’t find anything to commit to.

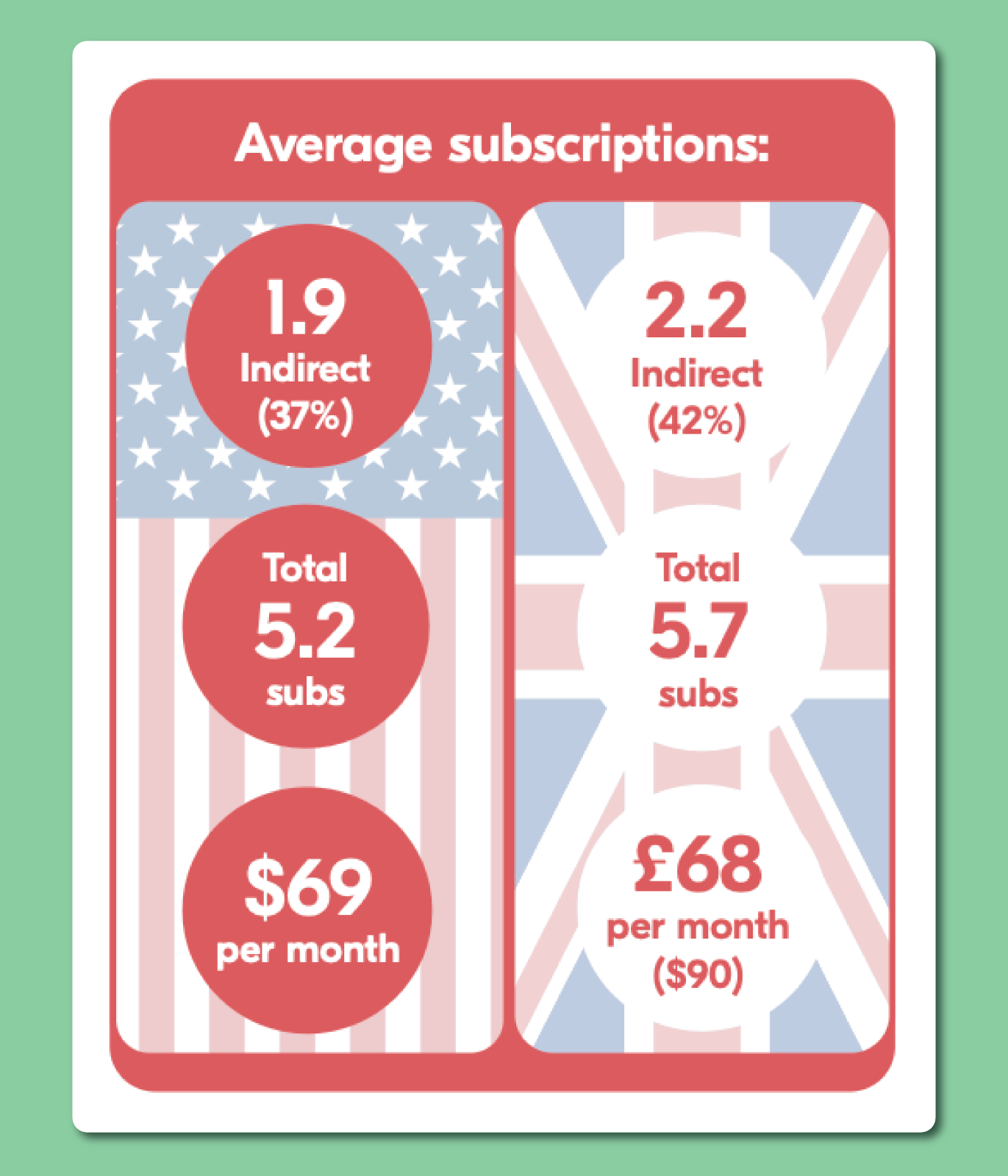

The same pattern shows up in how subscriptions are managed. In the US, consumers now hold an average of over five subscriptions and spend $69 a month, highlighting how deeply subscriptions have become part of everyday life. People continue to sign up, stay subscribed and use multiple services at the same time, so on the surface the model still appears to be working as intended.

What is changing becomes clearer when you look at how those subscriptions are actually being used.

Instead of sticking with one service over time, people dip in and out depending on what they need, adjust their plans when prices shift and increasingly access subscriptions through bundles or shared access rather than going direct.

When these behaviors are looked at together, they begin to point in a different direction, where the connection between subscriber and service is no longer the centre of the experience in the way it once was.

Subscriptions don’t always start with a direct sign-up

Not every subscription starts with a direct sign-up anymore. Rising prices and too many services are pushing people to find ways to keep access without overspending.

That might mean moving to a cheaper plan, accepting ads or continuing to share access even when services try to prevent it. Around 36% are now willing to accept significantly more advertising if it lowers the cost, a sharp reversal from 2024 when 78% said they strongly objected to paid subscriptions with ads.

At the same time, subscriptions are increasingly picked up in a different way. In the US, consumers now hold an average of two subscriptions through bundles, deals or third-party providers.

Access often comes as part of something else, whether that is a mobile plan, a broadband package, or another service in between. What used to be a direct path between subscriber and service becomes less visible and the moment of sign-up is no longer where the relationship is defined.

Discovery and loyalty extend beyond the platform

More than half of consumers (59%) now say they are loyal to the shows they follow rather than the platform that delivers them and many cannot recall where they first watched a title. What stays with them is the content, while the platform becomes one of several steps in how they find and return to it.

That shift becomes clearer when looking at how people associate content with platforms. In the UK, only 18% correctly identified HBO Max as the home of Game of Thrones and House of the Dragon, while more than half placed it on a different service, often naming Netflix instead. Even for flagship titles, the connection between content and platform is not always front of mind in the way it once was.

At the same time, the volume of content is changing how decisions are made, with consumers spending longer choosing what to watch than actually watching and often moving on from shows early despite having more options than ever.

Around 22% would consider letting AI decide what they watch, rising to 40% among Gen Z, while a similar share would allow AI to manage their subscriptions entirely, with 20% willing to go further and let AI automatically subscribe, manage and cancel services on their behalf.

Discovery is no longer something that happens inside a single platform, but across recommendations, bundles and AI tools that increasingly shape what gets chosen before a service is even opened.

Growth is moving toward distribution, not just acquisition

Consumers are spending less time managing individual services and more time accessing them through bundles or offers that sit alongside something they already use, whether that is a mobile plan, a broadband package or another service that brings subscriptions together in one place.

This shift reflects a growing expectation that subscriptions should be easier to access and manage, without needing to sign up, cancel and reconfigure each service separately, particularly as the number of subscriptions continues to grow, with 31% of Americans now saying they are done with standalone subscriptions, rising to 48% among Gen Z.

For subscription providers, this does not mean the audience is shrinking, but that it is being reached through different routes, as access increasingly happens through partners, platforms and intermediaries rather than through direct sign-up alone.

For telcos, banks and other resellers, subscriptions become a way to simplify that experience, reduce cost and bring multiple services together, creating a stronger role in how people access and manage what they use.

Over time, growth becomes less about acquiring each customer directly and more about being present wherever access is already being shaped, which is where decisions are increasingly made.

What this means in practice

The subscription economy is still growing, but it is now shaped across bundles, platforms and intermediaries rather than a single point of entry.

Access sits in more places, which means being present wherever decisions are made matters just as much as what you offer within your own service.

Growth is no longer defined by owning the customer relationship end to end, but by being present wherever access is already being shaped.

The opportunity now sits with those who can make subscriptions easier to find, easier to manage and easier to access, wherever that decision happens. Download the full report to see what’s driving it and where it leads next.